If you're like most sellers, your gut instinct is to shy away from seller financing. when you hear you may have to “seller finance” the sale of your business, it can create confusion and skepticism.

Your first reaction is most likely “How does it work?” and “Why would I do that?”

At this point in your career, you are probably ready to sell your business, transition the operations to the new owner, and begin the next stage of your life. So why would you still keep skin in the game?

We have counseled hundreds of business owners through selling their business and getting the highest value for it. We’ve seen that in some cases, seller financing a portion of your sale can help you get the best deal for your business.

In order to best help you (whether you work with us or not) we created this article to go over what seller financing is and why it may be required in the sale of your business. After reading this, you will have a clearer idea of whether you will or will not need to seller finance a portion of your sale.

Let’s begin.

What is Seller Financing?

Seller financing is when a business owner acts as the lender for all or a portion of the sale of their business. The buyer will be responsible for paying them back in the same way that they would pay a traditional lender.

Most sellers will try to avoid seller financing because they want the sale proceeds immediately. However, that is not always possible depending on the buyers interested in your business.

According to Guidant Financial, 60% - 90% of small business sales involve some form of seller financing.

Seller financing can be referenced in many ways:

- A seller note

- Seller carry

- A purchase money note

- Owner financing

By offering to finance a portion of your sale, you can attract more buyers and increase your chance of selling for the price you want.

Although seller financing has its positives, it does have its negatives too. You should consult with a merger and acquisition (M&A) advisor or deal attorney before considering offers for your business.

Two Main Examples of Seller Financing

We’ll go through two examples of seller financing to show how it is used in a transaction. Don’t worry if your business is smaller or larger than the example - the fundamentals of how seller financing works will be the same.

1. Finance The Majority of The Purchase Price

For businesses that are too small to use the SBA 7(a) loan program, have very messy financials, or otherwise don’t qualify for a bank loan, buyers will often try to seller finance the entire purchase price.

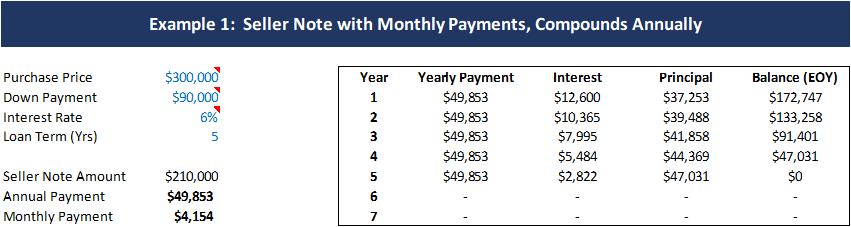

Say you’re the owner of ABC Company, Inc. You’ve been operating for many years with consistent revenue around $500,000. Your profit margins have been solid at 20% and you worked with a business broker who valued your business at around $300,000.

The first offer you receive is for $300,000 but the buyer wants you to finance the full purchase price.

Want to calculate your own seller note using this calculator?

Download our Seller Note Amortization Schedule Maker Here:

This means the buyer will pay you a down payment at closing and you’ll “carry” the rest as a promissory note. A typical down payment might be 25% to 50% depending on the size of the transaction.

This promissory note will usually have an interest rate associated with it in the range of 4% to 8%. Seller notes are typically over 3 - 6 years but it is also common to have a balloon payment, much like a commercial real estate loan.

In this deal, you agree to a 5-year term with no balloon payment.

In our example, you and your broker negotiate a $90,000 down payment (30%) and an interest rate of 6% per year, compounded annually. It is not uncommon for the interest rate to compound monthly like a home mortgage but it is open to negotiation.

So, how much money do you put in your pocket and when?

At closing you’ll receive the $90,000 down payment and then for 5 years you’ll receive monthly payments of $4,154.

2. Serve as a Supplement to a Bank Loan

The most common use for seller financing is as a supplement to an SBA 7(a) bank loan. In this instance, the buyer will get a bank loan for the majority of the purchase price and a smaller note from the business owner. For this, a typical seller note might be 5% - 15% of the total purchase price.

In most cases, the SBA lender will want the business owner to offer some form of seller financing. Using seller financing can help the debt service coverage ratio, or the ratio of business income to loan payments, which makes getting financing easier.

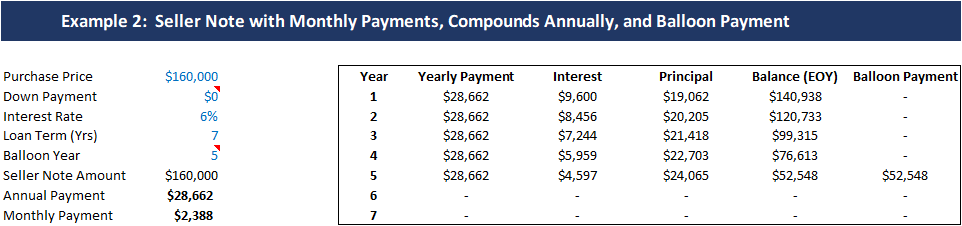

Say you’re now the owner of DEF Corp. and you’ve started working with a broker to sell the company. DEF does about $3,700,000 in revenue and earns $500,000 in Seller’s Discretionary Earnings (SDE). The broker you’re working with suggested a list price of $1,750,000 to leave room to negotiate.

After some back and forth, you and the buyer settle on a $1,600,000 purchase price with a seller note of $160,000 (10%). The buyer will get the rest of the purchase price through an SBA 7(a) loan.

You also agree that the seller note will be amortized over 7 years with a balloon payment in 5 years. This means the buyer will pay you the outstanding balance of the loan at the end of the 5th year.

At closing, you’ll receive $1,440,000 and have an outstanding seller note of $160,000. For this loan, you’ll receive payments of $2,388 per month for 5 years and a balloon payment of $52,548 at the end of the 5th year.

The Purpose of Seller Financing in the Sale of a Business

The Benefits The Buyer Receives From Seller Financing

Seller financing is highly advantageous for buyers. Here are the top benefits:

- It makes it easier to get an SBA loan

- It can serve as an alternative to SBA financing

- It can help strengthen your offer or allow you to do deals you otherwise couldn’t

The Benefits The Seller Receives From Seller Financing

Just like seller financing can benefit the buyer, it can also benefit the seller by:

- Offering tax advantages by spreading out the payments you receive

- Allowing potential for interest at an attractive rate

- Making the deal possible or helping you get the price you want

Business owners who are willing to seller finance all or a portion of the sale show the buyer that they are confident in the company’s current state and future.

The Disadvantages of Seller Financing in a Business Sale

Although there are benefits to both the buyer and seller when it comes to seller financing, there can also be disadvantages:

- The risk for the seller increases when they sell completely through seller financing

- It can put the long-term relationship of the buyer and seller in jeopardy if it goes awry

- The seller doesn’t receive their proceeds until years after the sale

If you are the seller, you should consider a few things before accepting an offer with a seller note.

Always do your due diligence on the buyer - including a credit check and background check. You should also call references regarding their character.

Sellers who finance the entire sale will be the only lender and will be in the first position if the buyer defaults on the loan. Since the seller is in the first position, the seller will need to file a UCC lien on all assets to protect them.

If a lender is involved in the sale, the lender will be in the first position and the seller will be in the second position. In this case, the lender will file a UCC on assets since they are in first position.

If you are a seller considering seller financing, you should consult with a trusted broker or M&A advisor to learn how to do it in a way that protects you and the business if the buyer defaults.

Determine if You Want to Seller Finance Your Business

Ultimately, it is up to you whether you will seller finance all or a portion of the sale price when selling your company.

You will need to consider the value and structure of your business to see if seller financing would help you get the best deal when selling.

Business brokers and merger and acquisitions advisors are the best professionals to consult with when determining if you should seller finance because they have experience with structuring business sales.

To learn more about how seller financing works, check out our page on Seller Financing or give us a call today to see if it is the best option for the sale of your business.

Know Your Company's Worth

Prepare to sell by determining the value of your business.

Subscribe To

THE MIDSTREET BLOG