With so many finance terms and acronyms floating around, it can be difficult to keep track of what they all mean. Perhaps even more difficult is keeping track of which ones actually apply to you.

One of these acronyms you’ve probably heard before is EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization).

If you own a business with more than $1 million in earnings, there’s a good chance your business will be valued using EBITDA.

You may have just wrapped your head around what EBITDA is when your M&A advisor or business broker starts using the term “adjusted EBITDA.”

It can get confusing, I know.

Luckily for you, MidStreet has performed thousands of valuations and worked with hundreds of business owners to calculate their adjusted EBITDA when selling their businesses.

In this blog, we’ll offer a brief refresher of EBITDA, offer a definition of adjusted EBITDA, and point out a few things to keep in mind when your business’s EBITDA is being adjusted.

Let’s hop in.

Adjusted EBITDA Defined

Adjusted EBITDA is a metric of a business’s earnings that starts with net income and adds back interest, taxes, depreciation, and amortization expenses, along with non-recurring and discretionary expenses in order to give a clearer picture of a company's earnings.

We’ll get back to adjusted EBITDA shortly, but first, let’s refresh your memory on what EBITDA is. If EBITDA is already familiar to you, you can click here to skip down to the Adjusted EBITDA section of this blog.

What is EBITDA

Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) is a metric of valuation generally used to value companies with more than $1 million in earnings.

There isn’t necessarily a hard and fast rule for when EBITDA should be used instead of SDE because several factors—such as owner involvement and types of buyers – determine which metric is best for each business.

To learn more about the difference between SDE and EBITDA, check out this resource.

EBITDA is calculated by removing certain expenses (interest, taxes, depreciation, amortization) that won’t necessarily transfer to a new owner.

_WebP-1.webp?width=542&height=575&name=EBITDA%20Formula%20(2)_WebP-1.webp)

You may be wondering why these items are added back to calculate a business’s value. Let’s quickly explain why each of these adjustments are necessary when valuing a company using EBITDA.

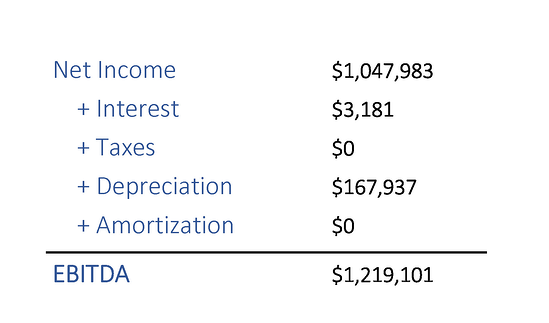

Net Income – Your net income is the starting point for calculating EBITDA.

Interest – Even though the new owner will have interest expenses, they can choose if they want to use debt to finance the business and negotiate their terms for it.

Taxes – Taxes are added back to the net income so the business’s earnings can be compared to others with different structures and tax brackets. Your taxes may be more expensive than another owner’s, so it’s added back to create an apples to apples comparison.

Depreciation and Amortization – Depreciation and amortization are useful primarily for tax preparation. They are added back because they are a non-cash deduction, and a new owner will have their own depreciation and amortization schedules.

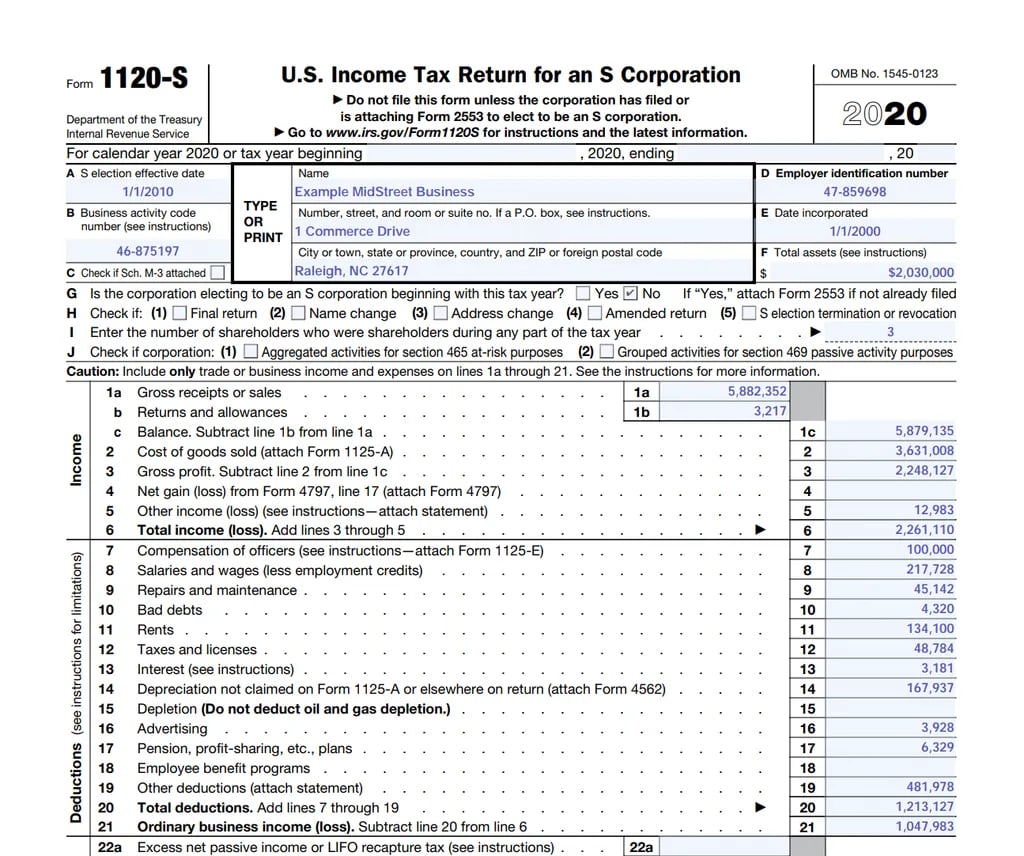

To give you an even clearer understanding of how EBITDA is calculated, check out the example income tax return for an S Corporation valued using EBITDA below.

For a further explanation of this sample valuation, check out our blog "What Is EBITDA? (with Formula)."

- A Note on Taxes: If you are tracking any form of income taxes on your Profit and Loss Statement, this expense can be added back to EBITDA (including state income taxes being written off on your federal returns, known as "Pass Through Entity Tax"). That said, if you are not expensing any form of income taxes, there won't be an add-back.

Adjusted EBITDA

Now that you’ve been refreshed on what EBITDA is and why it’s used, let’s talk about adjusted EBITDA.

Adjusted EBITDA starts with EBITDA and adds back even more expenses to more accurately represent the earnings of your company.

These additional add-backs may be an owner’s discretionary expenses, or any one-time (non-recurring) expenses that aren’t required for the business to operate on a regular basis.

You’ll want to use a trustworthy M&A advisor or valuation expert when calculating your company’s adjusted EBITDA. Some professionals can get a little too creative when they make add-backs to your business’s earnings, which can mislead you on how profitable your business actually is.

Remember, the purchase price of your business is directly related to how much earnings it creates.

Valid Add-Backs

While you can’t go adding back every expense to your earnings, there are some that are entirely valid, and should be added back to give buyers a clear understanding of how your company compares to others, and what its earnings truly are.

Some of these valid add backs, which can be positive or negative adjustments, include:

- Excess owner’s salary: Sometimes owners will pay themselves more than the market amount for their role in the business. With adjusted EBITDA, you’ll adjust the officer's salary to be a market rate for a manager if they were to replace the owner’s role. For example, if you pay yourself $300,000 for your role in the business, but another owner could replace you with a manager who is paid $200,000, then $100,000 (the excess) would be added back.

- Discretionary expenses of the owner: Many owners we’ve worked with run discretionary expenses through the business that might not continue with new ownership, including owner’s health insurance, personal auto expenses, family member salaries, travel/entertainment, and vacations.

There are also valid one-time expenses that should be added back, such as:

- Moving expenses: If a company changes locations, there will likely be some hefty expenses associated with the move. Since the move isn’t a regular expense, it should be added back to the net income.

- Remodeling: Remodeling, if not capitlized on the balance sheet, is generally not a recurring expense. Since a new owner won’t incur any remodeling expenses (unless they choose to) this is also a valid add-back.

- Non recurring business improvements: Sometimes business owners choose to revamp their website, branding, hire an outside accounting firm to clean up their books, etc. This is not a necessary expense to operate the business and shouldn't necessarily impact Adjusted EBITDA calculations. These types of add-backs will need to be carefully considered on a case by case basis.

- Charitable Donations: While charitable contributions are admirable and generous, they aren’t a necessary expense, making them a valid add-back.

- Litigation Expenses: Generally speaking, a business doesn’t undergo enough legal trouble for litigation expenses to be considered recurring, so these add-backs are usually valid.

Common negative adjustments we see:

- Other income: Any income not related to business operations that are not expected to continue should be subtracted from EBITDA. The most common examples we see are ERTC or PPP Income, gain on the sale of an asset, or interest.

- Below market rent payments to your LLC: If you pay yourself too little in rent, rent will have to be increased to a market rate, thus reducing the EBITDA.

Invalid Add-Backs

While the items listed above are generally accepted as valid add-backs (as long as they are reasonably explainable) there are some invalid add-backs that valuation experts or business brokers could try to include to inflate the EBITDA.

Some of these include:

- Adding back Section 179 as an expense: We’ve seen brokers in the past add back section 179 as if it was an expense. In reality, section 179 is a tax return item and does not flow through your P&L statement. Adding it back would inflate the earnings of your company improperly.

- Adding back the entire officer’s salary amount and not factoring in a manager’s salary: Some brokers may do this when calculating adjusted EBITDA because they’re used to following add-backs for SDE. This is not an accurate add-back because companies valued using EBITDA won't be owner-operated, so a fair-market-value salary (to be paid to a hired manager) is more appropriate. For example, an owner may be paying themselves $200,000 when a fair-market salary is only $100,000. Adding back the full $200,000 rather than the fair-market salary inflates the valuation by $100,000.

- "Add backs" that only impacts the balance sheet: The most common culprits include, financed car payments, owner distributions, or one-time equipment purchases that are capitalized instead of expensed. If you're worried you might make this mistake, an easy check is to ensure what your adding back is actually an expense. You can't add-back expenses that never impacted the profit and loss statement.

- Failing to remove the Employee retention tax credit: The employee retention tax credit was a federal program under the CARES act designed to encourage businesses to keep employees on their payroll. Many businesses have taken advantage of this useful provision, but it needs to be factored out of the earnings of the company.

- Adding in buyer synergies: Calculating your expected buyer synergies into your adjusted EBITDA is a very difficult task, and most buyers are unwilling to consider adjustments of that nature. That does not mean, however, that you can't get credit for selling to a buyer who can take advantage of synergies with your company. Generally, you get credit through a stronger multiple assuming there's competition and the buyer is compelled to pay what they are able to pay.

Understanding Adjusted EBITDA

Adjusted EBITDA is one of the most common metrics to help business owners and business buyers compare companies’ earnings by adjusting for one-time expenses, discretionary expenses, and other expenses that will likely change under new ownership.

To determine the true value of your company, you’ll want to hire an experienced business broker, M&A advisor, or valuation expert to determine your company’s EBITDA and make the appropriate adjustments.

Now that you know more about how adjusted EBITDA is calculated, you’ll have a better understanding of how the professionals you hire determine the value of your company.

For more on how businesses are valued, check out our blog “What Is a Business Valuation? (And Which Type Is Right For You?)” and “What Multiple Should You Use to Value Your Business?”

These are both great resources that provide examples of add-backs and the comps reports that help determine a range of multiples for your business’s EBITDA.

To learn more about business valuations and have one performed on your company, contact us today. We’d be glad to explain our process and offer a free business valuation.

Know Your Company's Worth

Prepare to sell by determining the value of your business.

Subscribe To

THE MIDSTREET BLOG