What is Seller’s Discretionary Earnings?

Seller's Discretionary Earnings, or "SDE", is a financial metric used to determine the true historical benefit to the owner of a small business.

Calculating SDE is a way to standardize or "normalize" a company's earnings so it can be more accurately compared to the earnings of other companies and the industry as a whole.

If you own a small to mid-size business, it's important to have a good understanding of the meaning of SDE and how its calculated. By doing so, you'll gain a better understanding of your business' true earnings, an accurate picture of its value, and insight on things you can do to enhance its value as you move forward.

In this blog, I'll more fully answer the question "what is SDE?", explain how SDE is calculated, and finish by showing a real-world example of how you can normalize, or "recast" the financials to calculate the SDE in your business.

Let's jump in!

Definition of Seller’s Discretionary Earnings

Seller's Discretionary Earnings is a measure computed for a small to mid-size business that starts with the net profit, then adds back interest, taxes, depreciation, and other adjustments to show the entire financial benefit provided to one full-time owner-operator.

The International Business Brokers Association (IBBA) defines SDE as:

"The earnings of a business prior to income taxes, depreciation, amortization, interest, non-operating income and expenses, nonrecurring income and expenses, one owner's entire compensation (including benefits and any non-business or personal expenses paid by the business)."

Why Is SDE Important?

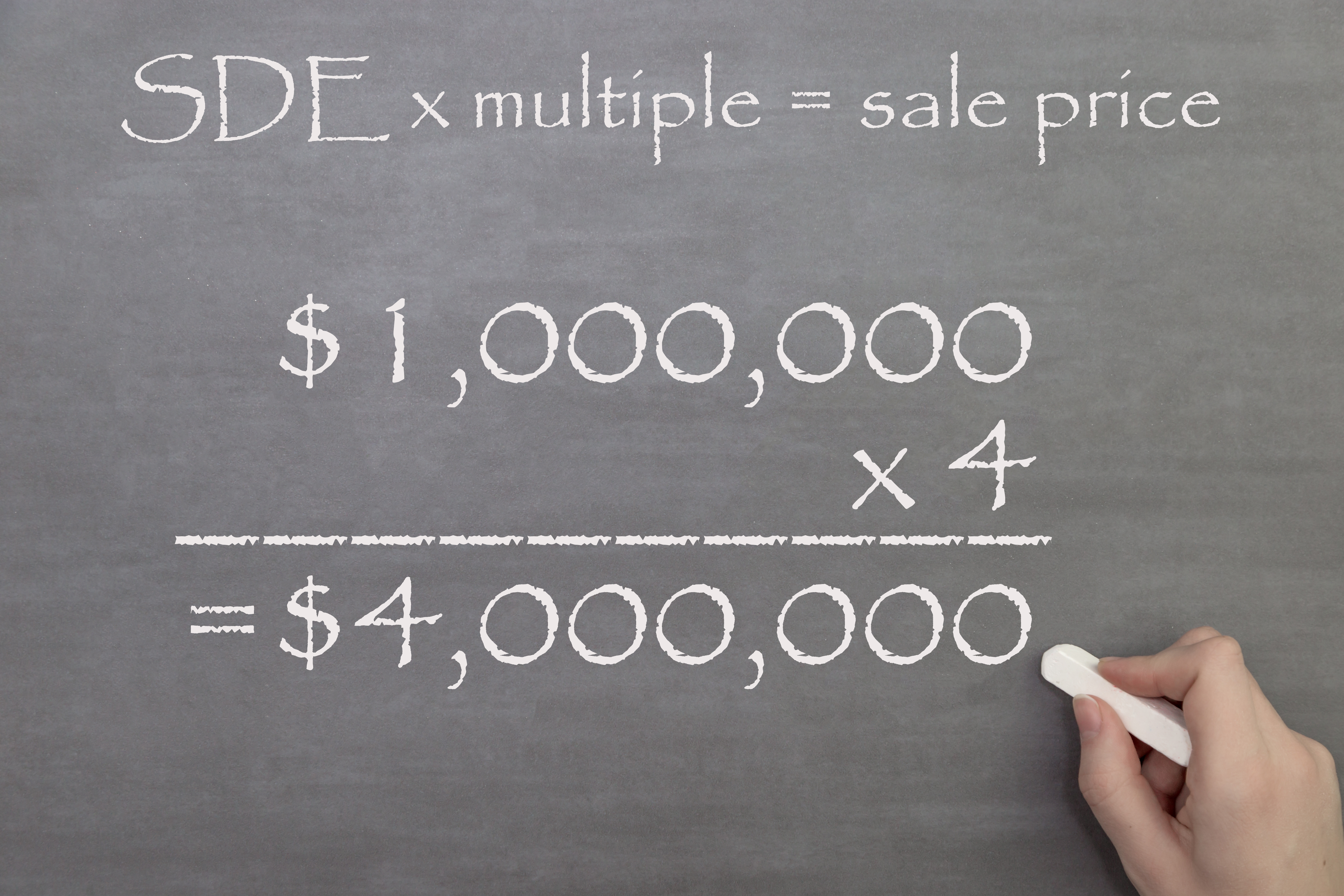

There are a number of ways to value a business, but the most commonly accepted valuation method involves applying a multiple to a company's earnings.

Here's the problem...

Unless you're one of the rare few who enjoys paying taxes, you've been working with your bookkeeper and/or CPA to make sure your bottom line stays as low as possible.

There's nothing wrong with taking every legitimate tax deduction, but it does present an issue when it comes time to sell.

Buyers looking to acquire your business want to know:

1. "How much money would I be able to put in my pocket?"

2. "How do the price and earnings of this business compare to other, similarly-sized businesses?"

Valuing a business is much different than valuing things like a home or car. No two businesses are exactly alike - even businesses of the same size in the same industry will have their own unique set of books.

And determining an accurate picture of your company's value isn't possible unless it can be compared to similar companies that have sold in the past.

That's where Seller's Discretionary Earnings come in.

SDE helps compare the true profit of your business to others by "recasting" or "normalizing" its financial statements. Once your business' true earnings have been calculated, your business can then be compared to other similar businesses that have sold in the past.

Comparing your business to others that have sold is called the "market method". The market method is performed in much the same way as it is in a real estate appraisal.

For example, to determine the value of a 3 bedroom, two bath house, a real estate agent would start by looking at other 3 bedroom, two bath homes that have sold nearby. This is known as the "comparable sales method".

While determining the value of your business is much different than getting an appraisal on your home, the comparable sales method is often the most accurate valuation technique for both.

When determining the value of your business, a business broker, M&A advisor, or business valuation analyst surely use the comparable sales method. They will research industry databases to find use find as many comparable businesses as possible. By knowing the sales price and SDE, they can find the determine the "SDE Multiple".

Here is an example:

- Business Sales Price: $1,200,000

- SDE: $350,000

- SDE Multiple: $1,200,000 divided by $350,000 equals 3.42

So, if your business was similar to the one used in our example, and your SDE was $450,000, you could reasonably assume your business would be valued at approximately $1,500,000.

- $450,000 x 3.42 = $1,539,000

So, to summarize, SDE is an important metric you need to understand and have the ability to calculate. It is one of the only ways prospective buyers (and their lenders and investors) will be able to estimate your business' cash flows and more accurately compare your company to others.

Calculating Seller’s Discretionary Earnings

As we discussed earlier, calculation of your SDE starts with your net profit.

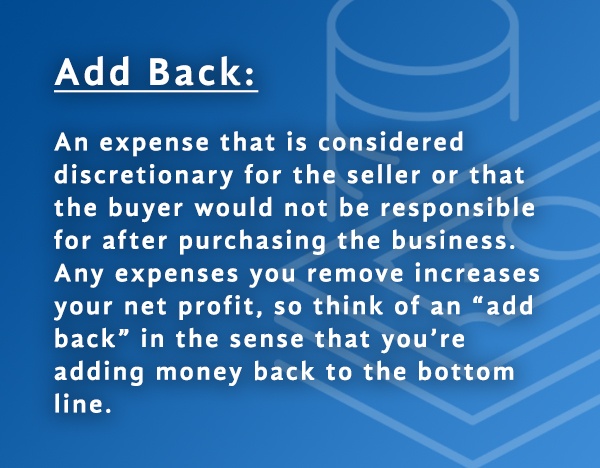

Then, adjust or "recast" your financials by identifying items that should be added to, or deducted from, your net profit. These adjustments are known as "add-backs".

An add-back is defined as all, or a portion of, the expenses added back to net income in an effort to place the figures as close as possible to the true economic earnings actually derived from the business.

Types of Add Backs

In general, add backs fall into one of five categories:

- Standard

- Discretionary

- Non-recurring

- Non-operating

- Accounting adjustments

These items will vary from company to company, but understanding these major categories is helpful in identifying potential increases to, or reductions from, your business' SDE.

Standard

Here are the most commonly accepted add-backs:- Salary for one full-time owner

- Owner's payroll taxes

- Depreciation

- Amortization

- Interest

Discretionary

Discretionary add backs are expenses that don't necessarily contribute to the operating performance of your company or are unlikely to continue under a new owner.

Examples include:

- Personal travel

- Personal or family member fuel

- Club dues

- Owner's health insurance

- Personal or family member mobile phone

- Charitable contributions

Non-recurring

One-time or non-recurring add backs are expenses unlikely to occur again in the future. You may also hear these referred to as "non-recurring expenses".

Examples include:

- Legal, consulting, or other professional fees

- Transaction-related costs

- One-time technology upgrades

- Facility relocation expenses

- Equipment repair/replacement/upgrade

- Bad debt expense

Accounting Adjustments

Additional accounting adjustments may be necessary to reflect your true earnings. These adjusts may add to, or subtract from, your profit.

Examples include:

- Non-operating income (i.e.: the sale of a vehicle or piece of equipment)

- Inventory adjustments

- PPP loans

- Below-market rent

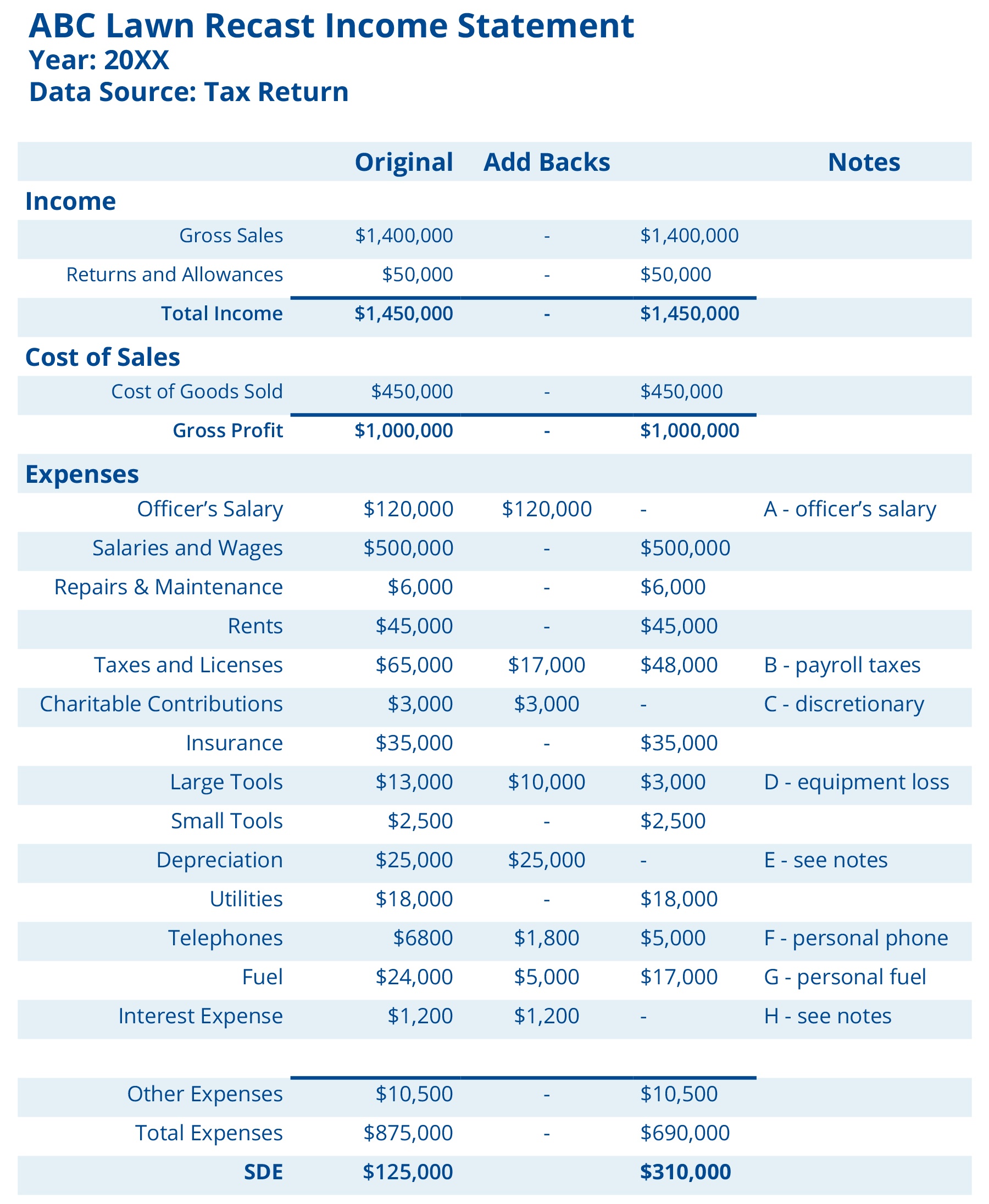

SDE Calculation Example: ABC Lawn

Now that you have a base-level understanding of common add-backs, let's jump into an example.

- ABC Lawn has decided to get a valuation on their business.

- The company has one owner, who takes a salary of $120,000 per year and works full-time in the business (A).

- This year, the owner had to replace $10,000 worth of equipment when a water line broke and flooded the warehouse (D).

- The company is paying for a cell phone plan that includes family members of the owner (not currently employed by the business). (F)

- The owner's family members are using a company fuel card to fuel their vehicles (G).

NOTES:

A – Officer’s Salary is added back to show what one full-time owner-operator can receive from the business. Note: If multiple owners participate in daily operations, add back one full-time owner and adjust the expenses to an amount equal to what it would cost to hire an employee/s to replace the additional owners.

B – Company's share of owner's payroll taxes are added back

C – Charitable contributions are not critical to operation of the business

D – Non-recurring expense of equipment damage is added back into net profit

E – Buyer will have their own depreciation schedule

F – Personal telephone bill added back

G – Personal fuel expense added back

H – Buyer won’t be paying same interest

Study the example above and use it to help you calculate your own Seller’s Discretionary Earnings.

If you’re having trouble identifying add backs relevant for your business or you’re confused on any step in the process, please feel free to reach out. We’d be more than happy to help.

What’s the difference between SDE and EBITDA?

For larger businesses, "EBITDA" is used in place of SDE.

EBITDA stands for earnings before interest, taxes, depreciation, and amortization.

EBITDA is very similar to SDE and, when calculated for the purposes of valuing a business, add-backs are performed in much the same way.

There is one major difference. When calculating SDE, an add-back is made for one full-time owner operator. EBITDA does not allow for an add-back of the owner operator salary. Instead, the salary, or salaries, necessary to operate the business are included in the expenses.

Why? For larger businesses, it is assumed the owner, or owners, are taking on more of an investor role and not participating in day-to-day operations of the business.

Even if the seller is actively involved, a buyer will be most likely looking to operate the business with a manager. That means the manager salary must be included in the expenses to show the true earnings of the business.

To arrive at a basic calculation of your adjusted EBITDA, simply follow the steps shown above for SDE, then include in your expenses what it would cost to employ someone to take over your daily responsibilities (if you're currently an owner-operator).

Keep in mind, the amount you use for a manager is a market rate and not necessarily what you're currently paying yourself. Depending on the size of your company, this adjustment can be as little as $75,000 or as much as $200,000 or more.

To learn more, take a look at our blog on the differences between EBITDA and SDE.

Know Your Company's Worth

Prepare to sell by determining the value of your business.

Subscribe To

THE MIDSTREET BLOG