Do you want to know the steps to selling your small business?

Maybe you've received an offer from someone interested in purchasing your company.

Or perhaps you're just interested in learning more about the process.

Look no further - this is a guide on how to sell your business from start to finish.

Selling a business is usually a long and emotional process that involves a good deal of preparation.

Be prepared to spend six to eleven months on the sale.

Your satisfaction with the result depends on:

- The reason for the sale

- Your level of preparation

- The quality of advisors you select

- The buyer you choose

Step 1: Prepare to Sell

The first step in the process is to answer this question: Why do I want to sell my business?

Here are some common reasons we see:

- Health problems and burnout

- Retirement

- Divorce

Plan for what you’re going to do after the sale of your company, whether that means moving on to another venture, focusing on family life and hobbies, or even volunteering in your community.

When preparing to sell, focus on the factors that will make your company more valuable, such as:

- Reducing your day-to-day involvement

- Eliminating unnecessary expenses

- Cutting down on customer or supplier revenue concentration

Step 2: Set a Price

A MidStreet business ($1M-$25M in revenue) will usually sell for 2-6 times profit, depending on its profitability, size, industry, type of buyer, and several other factors.

You have three options for pricing the business.

- Create a ballpark price range on your own

- Pay for a business appraisal

- Engage a business broker to perform a business valuation

Once the valuation is complete, work with your accountant to see how much money you would walk away with. This exercise will help you decide if now is the right time for you to sell.

Also, decide if you’re interested in selling your company’s real estate.

Step 3: List with a Business Broker

Would you review all your legal documents yourself, or do you hire a lawyer to represent you?

Similarly, when the time comes to sell your business, enlist the help of a qualified business broker dedicated to helping you achieve your goals.

Quality brokers earn their fee by providing value throughout the sale.

In a negotiation, a simple conversation between the broker and the buyer could mean the difference between you gaining or losing $100,000.

What is the best way to find a quality business broker?

We recommend looking based on experience and accreditation.

You can also search the IBBA website by using the Find a Business Broker search tool and speaking with brokers who have their CBI (Certified Business Intermediary) certification.

Step 4: Gather Documents

It’s important to make a buyer feel comfortable by being prompt with their requests, and the best way to do that is by gathering documents in advance.

Here are a few items to gather upfront:

- Financial information (already gathered)

- List of equipment

- Permits and licensing agreements

- Corporate governance documents

Step 5: Find a Buyer

If someone has offered to buy your business unsolicited, it is unlikely that they will offer what the business is actually worth in the market.

If you want the best price and terms for your business, enlist an experienced business broker to handle the sale.

A broker will prepare a marketing package to help buyers better understand your business. The following items are typically included:

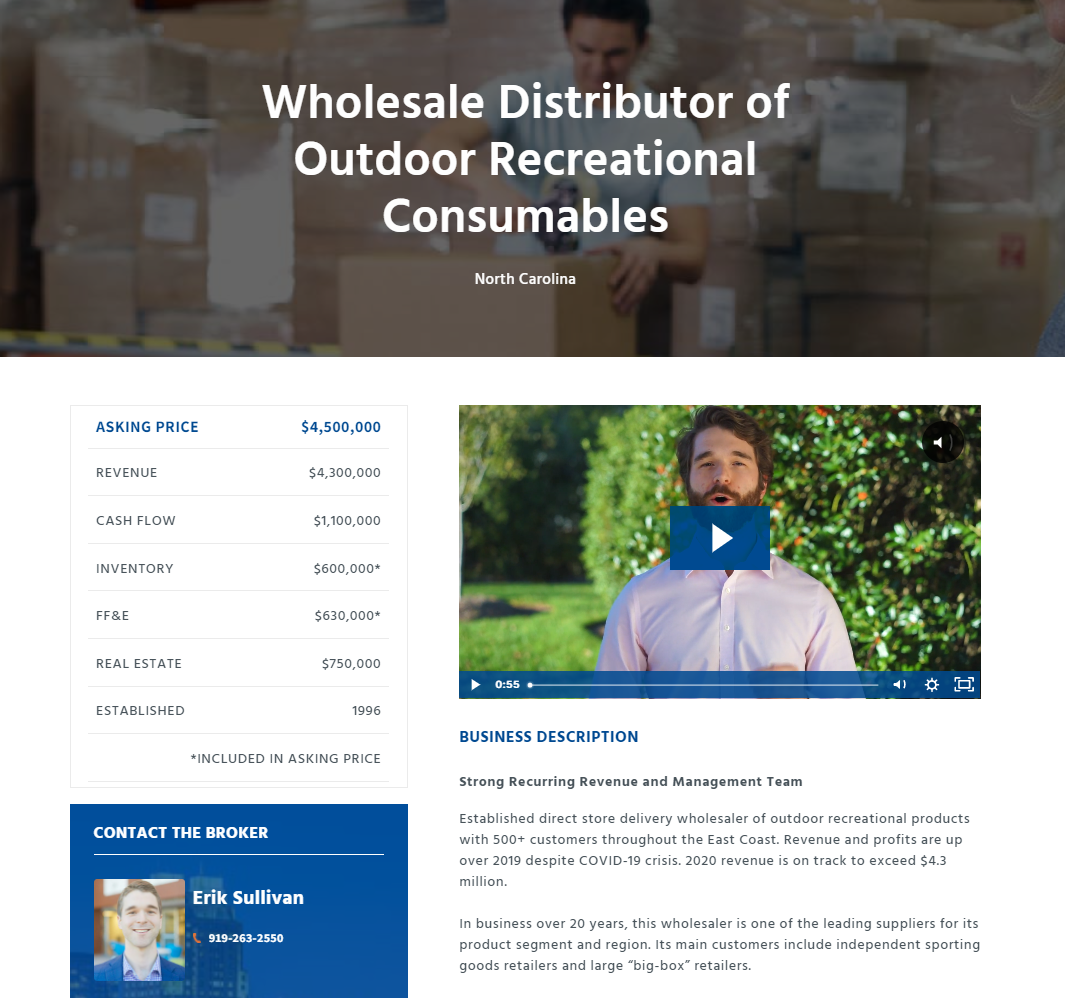

Blind Ad: Used to give potential buyers just enough information so that the best buyers will inquire about the opportunity. See an example from our website below.

CIM (Confidential Information Memorandum): A written summary of the business. These can be anywhere from 1-40 pages in length, depending on the brokerage.

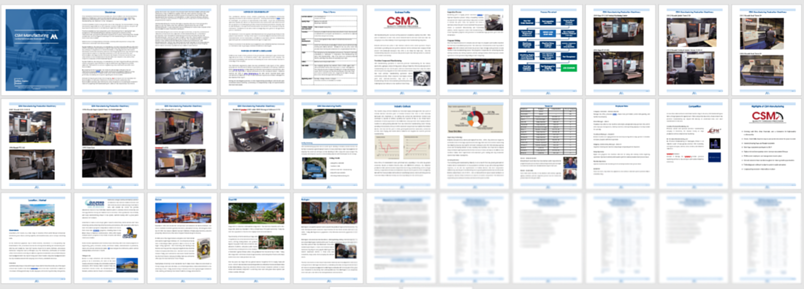

Marketing Video: Gives prospective buyers an “inside look” at your business. See an example we created for Mill Tek Toll Grinders below.

Once a buyer reviews the marketing materials, if they’re interested in taking the next step, the broker will likely set up an introductory call with you and an in-person visit for the best candidates.

Eventually, you will receive offers on your business.

Step 6: Accept an Offer

At this stage, you’ve marketed your business for sale and have received interest from buyers.

It’s time to receive offers and come to an agreement with one of the candidates.

Before you accept anything, think back to your goals with selling to determine what price and terms you’re comfortable with.

Below are documents that you’ll likely see as you move forward.

- IOI: Indication of Interest. A non-binding document usually covering only the basic financial terms of a deal.

- LOI: Letter of Intent. A document describing the intentions of the buyer in a potential purchase. Usually more detailed than an IOI.

- Purchase Agreement. The final, definitive agreement between you and the buyer.

After you accept an offer, you will enter due diligence.

Step 7: Due Diligence and the Purchase Agreement

Due diligence is a review performed by the buyer to confirm the facts you represented in your marketing materials and in follow-up conversations.

Until you trust the prospective buyer, avoid providing information that might put your business at risk, such as supplier contact information or detailed product ordering information.

During Due Diligence, the buy-side and sell-side (or transaction) lawyers should work together to complete the purchase agreement.

Step 8: Closing and Training

If the buyer is using SBA 7(a) financing, the lender will perform their own due diligence.

Work together with your broker and the buyer to satisfy all lender requests.

At the end of this process, you’ll meet the buyer, attorneys, and your broker in a conference room (or virtually!) to sign all of the required closing documents.

Once you've received the funds from the sale, now it's time to celebrate. Congratulations!

After closing, you’ll likely tell the employees you’re selling the business. I recommend introducing the buyer in the best light possible, to ensure a smooth transition.

Once the business sells, your level of involvement should be limited to training the new owner on running the business, as defined by the purchase agreement.

Prepare For The Journey of Selling Your Business

Selling a business is a long journey that demands perseverance and time.

It will require you to be emotionally ready and financially prepared.

But if you do it right and follow the steps outlined above, you could secure your family’s future and transition into the next chapter of your life.

Thank you for reading my post – email to jonah@midstreet.com with any questions, comments, or feedback.

Know Your Company's Worth

Prepare to sell by determining the value of your business.

Subscribe To

THE MIDSTREET BLOG