An asset sale occurs when the assets of your business are sold to a buyer.

When I refer to an “asset sale,” I am not talking about simply selling assets such as inventory and equipment.

You could sell your assets to an auctioneer and close up shop, but you wouldn't receive the money you deserve after years of successful ownership in your company.

Instead, I am referring to selling your business to a buyer who will take over its operations and pay you for its goodwill and hard assets.

Business owners often ask us about the benefits of an asset sale versus a stock sale, in which you sell the shares of your business.

For this article, we'll focus on understanding how to sell the assets of your business and why it matters to you as a business owner.

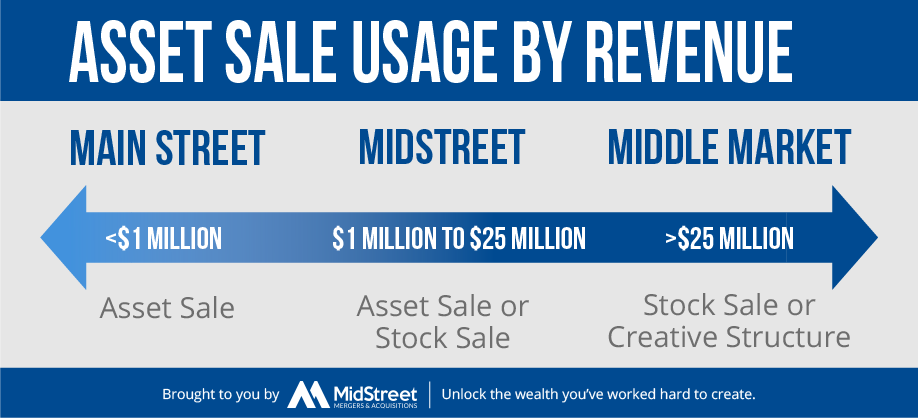

If you own a midstreet company ($1M-$25M in revenue), you might sell using an asset sale, a stock sale, or another creative structure.

Generally, as you go up in purchase price and the harder it is to transfer your assets, it becomes more likely to sell the stock of a business (see graphic below).

Disclaimer: This article is not intended as tax or legal advice. When considering an acquisition or sale and for tax planning purposes, I recommend buyers and sellers of businesses to consult with the appropriate professionals, including accountants and attorneys. Work with a quality CPA to determine your net worth after you sell your company.

Definition of an Asset Sale

In an asset sale, you (the seller) retain possession of the legal entity used to operate your business, and the buyer purchases the individual assets of your company.

In the final purchase agreement, the company's assets are broken out through an allocation of the purchase price into several buckets, including:

- Goodwill

- Equipment

- Inventory

- Training

- Non-Competition Agreement

- Real Estate (if applicable)

You'll pay taxes on each “bucket,” according to IRS guidelines. A common sticking point we see during negotiations between buyers and sellers is how goodwill vs. equipment are allocated in the purchase price.

For tax minimization, as a seller, you will likely want to allocate a greater value to goodwill than to equipment, since goodwill is taxed at the capital gains rate, while equipment is taxed at your higher income tax rate.

The buyer will want the opposite, since they can benefit from greater depreciation as described in the next section.

After the sale, you will also be charged normal income tax rates on the gain of your company’s assets, instead of their depreciated or book value. This is what is known as depreciation recapture.

The Buyer’s Perspective

By purchasing your business through an asset sale, a buyer achieves a “step-up” in basis of the company’s assets, allowing them to benefit from greater tax depreciation.

In addition to tax advantages, a buyer will likely not want to inherit your debts, liability for litigation, contract disputes, etc.

One of the downsides to an asset sale for everyone involved in the transaction is that certain assets can be difficult to transfer, such as contracts without assignability clauses or consent from a landlord.

Leverage the advice of a quality business broker, a transaction CPA, and an attorney to consider the buyer's perspective. Often, there is a way to achieve both your goals as the seller and those of the buyer through creative dealmaking.

Understand How an Asset Sale Works

How a deal is structured has a major impact on you (the seller) and the buyer.

Other factors beyond the scope of this article can also determine what structure you might use.

Before it is time to enter into a purchase agreement with a prospective buyer, you should seek advice from professionals with mergers and acquisitions experience.

That way, you can arrive at closing confident in your understanding of the taxes and liabilities that you will be responsible for after the sale.

If you have questions, comments, or feedback, email me at jonah@midstreet.com.

Know Your Company's Worth

Prepare to sell by determining the value of your business.

Subscribe To

THE MIDSTREET BLOG