When you think about how much your business is worth, it's easy to understand there is value in your equipment, vehicles, and tooling.

But what about all the years you've been in business? There has to be value in the reputation you've built, right? What about the business name, customer list, website, and employees?

All of these items are examples of the “goodwill” of your business.

Since these things are intangible, goodwill can be one of the hardest things to conceptualize in the sale of a business. If you can’t see it or measure it, how are you able to place a value on it?

Fortunately, there’s a step-by-step process to follow when calculating the goodwill of any business.

At MidStreet, we've spoken to hundreds of business owners about goodwill and how it affects the value and sellability of their company.

To help you understand what goodwill is in a business sale, this article will cover what goodwill is, how to estimate it, then discuss how it impacts the sale of your business.

Let’s hop in!

The Definition of Goodwill

In the sale of a business, goodwill is defined as the amount paid above and beyond the fair market value of the business' assets and liabilities.

For instance, some of the value of your business is in physical assets. For example, the vehicles and equipment you and your team use.

But if your business is like most, the value of your company is much more than the vehicles, tools, and equipment.

Most of your company's value is contained in intangible assets. For example, the company’s brand name, its reputation, or long-term customer relationships.

Goodwill is valuable to a buyer because it represents your company's ability to take physical assets and generate cash flow into the future.

If it wasn't for your company's goodwill, why would a buyer pay you above and beyond the market value for your vehicles and equipment? It would be more cost effective to just start a new business from scratch.

Example of How to Calculate Goodwill

During the sale of your business, one of the many items you and the buyer will negotiate is called the "allocation of purchase price", also known as asset allocation, or allocation.

Allocation is the process of dividing up the total purchase price into different categories, primarily for tax reasons. Goodwill is one of the items contained in the allocation.

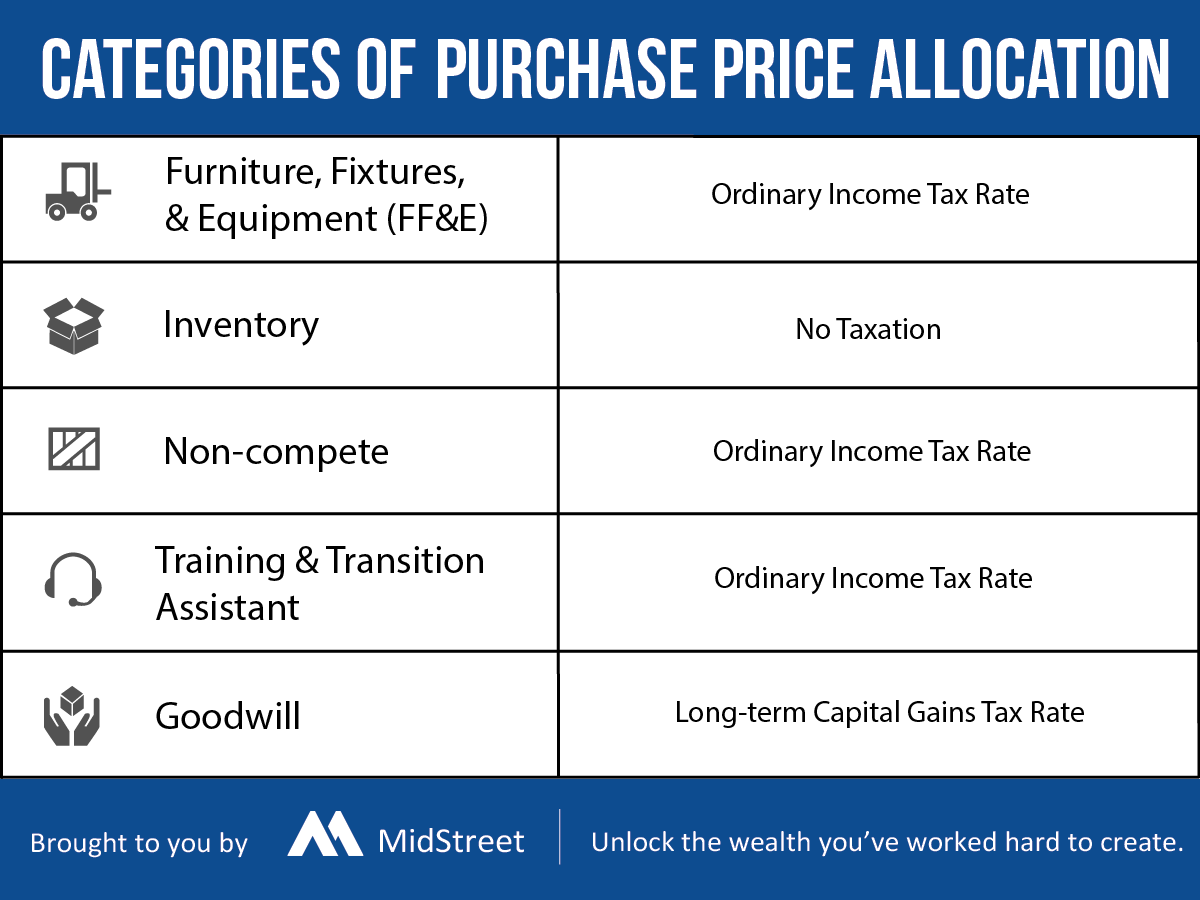

In most business sales, five categories are used in the allocation of purchase price:

- Furniture, Fixtures & Equipment (FF&E)

- Inventory

- Training

- Non-compete

- Goodwill

The way you calculate goodwill is by taking the purchase price and subtracting the other asset allocations.

To help illustrate, let’s go through an example.

Let's say you own a machine shop that does $1,800,000 in revenue and made $350,000 in Seller’s Discretionary earnings (SDE) last year.

You receive an offer for $1 million to buy your company.

Your business broker tells you it’s best to negotiate the asset allocation as early as possible because it greatly affects how much you’ll get to keep after taxes.

Since it also affects how the buyer will be taxed, it can become a point of contention during negotiations.

After some back and forth, you and the buyer agree to the following allocation:

Furniture, Fixtures, and Equipment: $250,000

The value of your machinery, tools, desks, chairs, computers, vehicles, and other hard assets used in your business.

Inventory: $100,000

The amount of in-stock raw materials or finished goods you will be leaving with the buyer. This value is determined at your cost, not what you sell it for.

Non-Compete: $25,000

You'll normally have to agree to a covenant not to compete with the buyer in a certain geography for an amount of time.

Training: $25,000

The value assigned to training and consultation which you will perform post-closing, included in the sales price.

Goodwill: $600,000

Goodwill is calculated by taking the total sale price of $1 million, and subtracting the sum of the other 4 categories.

By using the following equation, you can more clearly see how the value of goodwill is determined:

How is Goodwill Taxed in a Business Sale?

Note: Since asset sales are more common in lower middle market sales, we will only cover taxation of goodwill in an asset sale in this article.

If you’re a business owner, you know the tax man is waiting patiently for the day you sell your business.

Much like selling stocks, you’ll end up paying taxes on the gains you experience from selling your business.

The good news is, if you educate yourself early in the process, you may have the opportunity to reduce the total amount of tax you pay.

How?

First, it's important to understand goodwill is considered an asset. The goodwill has been building since your business was started.

Next, lets talk about long-term capital gains. Long-term capital gains are derived from assets held for more than one year before being sold.

As long as you've owned your business for more than one year, your goodwill will be treated as a long-term capital gain.

As the seller of a business, any amount allocated to goodwill is considered favorable.

Why?

Long-term capital gains are taxed according to thresholds which begin at 15% and graduate to 20%.

Amounts allocated to equipment, training, and non-compete are subject to ordinary income rates which can be as high as 37%.

How Goodwill is treated for the Buyer

Just like other assets, the buyer who acquires your business will be able to take a tax deduction for the amount of goodwill they received as part of the sale.

They can't write the goodwill off on their taxes all at once. Instead, they will be able to amortize it over 15 years, meaning they will write off 1/15th of the goodwill each year.

The amount of goodwill in the sale will be affected by the amounts allocated to other asset classes. If there is less allocated to the other assets, then goodwill will be higher. If there is more allocated to other assets, then the goodwill will be lower.

The buyer typically wants a low amount of goodwill and high equipment allocation.

You, as the seller, will want high goodwill allocation with less toward things like equipment and training.

Why?

- You (the seller) will pay more in taxes if the allocation to equipment is higher.

- The buyer will not be able to depreciate as much if the amount allocated to equipment is low.

In an asset sale, a buyer gets to step up the basis of assets. For example, say you as the seller bought a truck for $50,000 and then depreciated it to $0 over 3 years before the sale. That truck still has some service life left and the buyer will acquire it in the asset sale.

During the sale, a value needs to be allocated to that track - let’s say $25,000. Since you had previously depreciated the truck to $0, this would be a step-up in basis from $0 to $25,000.

After the sale, the buyer will have the truck on their balance sheet at $25,000, which means that they can depreciate it and receive the tax savings.

As the seller, you will have to pay ordinary income tax on the $25,000 that you received from selling the truck to “recapture” the depreciation you wrote off on your taxes.

Do All Businesses Have Goodwill?

All profitable businesses have goodwill unless the business has excessive assets. A business must generate a profit that justifies its assets. Your business may not have goodwill if:

- It is profitable but it requires a large amount of capital to operate

- You just started it and haven’t turned a large enough profit yet

- Your company has negative cash flow

If you own a machine shop that makes $250,000 per year in SDE (cash flow) but must own $10 million in equipment, there is not a goodwill balance. The purchase price of the business will be largely dictated by the equipment’s value.

Consider Goodwill in The Sale of Your Business

When you know how goodwill works and how it impacts your overall taxation, you can better prepare for your sale.

Allocations that are positive for the seller are usually neutral or slightly unfavorable for the buyer, while allocations that benefit the buyer usually disproportionately hurt the seller. Because of this, you should be prepared to make some compromises on the allocation of the purchase price but will want to hold a line.

Learn more about asset allocation in our article “What is Purchase Price Allocation in a Business Sale?”

We've helped hundreds of sellers choose the most beneficial allocation for the sale of their business. If you would like to learn more about how goodwill will be treated during the sale of your business, contact us today.

Know Your Company's Worth

Prepare to sell by determining the value of your business.

Subscribe To

THE MIDSTREET BLOG