If you're like most business owners, you don't love taxes. You don't have a choice but to pay them, but you wish there was a way to pay just bit less.

When the time comes to sell your business, you can be sure taxes will be a big part of the equation. If you haven't properly prepared, you may be very surprised the next time tax day comes rolling around.

At MidStreet, we've helped hundreds of business owners learn about the options available for their commercial real estate during a business sale. The most common include:

- Retaining the real estate and leasing it to the buyer

- Selling the real estate, then paying the appropriate taxes to free up cash

- Selling the real estate, then deferring all or a portion of the taxes by using a 1031 exchange to reinvest the proceeds

So, if you own the warehouse or office building your business operates out of, one of the primary tax strategies you'll want to take some time to learn about is the 1031 tax deferred exchange, or "1031 exchange".

The 1031 exchange is a powerful tool to help you defer your tax liability on the sale of investment real estate, including the sale of the real estate you own as part of your business.

In this post, we're going to cover:

- The fundamentals of a 1031 exchange

- Why it's important to a business owner who owns real estate

- The basic rules of a 1031 exchange

- An example 1031 exchange scenario for a business owner

- How to make (or break) your 1031 exchange – seeking qualified advice

- Frequently asked questions

- Resources for learning more

Disclaimer: Although effort has been made in providing accurate information, MidStreet does not warrant that accuracy and is not liable for any errors or omissions. MidStreet, nor its employees, are licensed tax professionals or attorneys. Readers are strongly encouraged to confirm tax and legal issues with accountants and attorneys in your respective state or province. The article is based on information as of summer 2020.

Fundamentals of a 1031 "Like-Kind" Exchange When Selling a Business

If you own the real estate associated with your business, you’ve likely experienced a gain in its value over time. When the time comes to sell, you’ll have to pay taxes on that gain. Here's the way that works:

Those taxes include depreciation recapture, federal capital gain tax, state capital gain tax, and potentially net investment income tax. Your tax professional can help you better understand your potential tax liabilities.

A like-kind exchange allows you to postpone those taxes if you reinvest the proceeds in similar real property.

For practical purposes, “similar property” means other real estate used as an investment, which would include real estate used as part of a business’s operations. However, it does not include personal property such as goodwill.

If you plan on selling your business and you own its real estate, you can perform a 1031 exchange on the company's real estate and sell the business to a buyer at the same time.

You could also sell only the business's real estate, without selling your business, and use a 1031 exchange to benefit from tax deferment while continuing to operate the business.

Make sure to seek qualified advice from a real estate attorney and identify a Qualified Intermediary well in advance of your closing date.

Benefits of a 1031 Exchange

Over the course of owning your piece of real estate, you’ve likely depreciated much of the value of the building, reducing many of the tax benefits of owning real estate.

Another major benefit of selling your property through a 1031 exchange is purchasing new real estate with a step-up in basis and deferring any depreciation recapture.

In other words, you can benefit from the new property’s clean slate depreciation schedule.

The step-up in basis is a powerful tax benefit of 1031 exchanges that the most successful real estate investors utilize regularly.

Below are some keywords and definitions to keep in mind that I’ll use throughout the rest of this post:

- “Taxpayer,” or “Exchanger,” the owner of the real estate – in this case, you.

- “Relinquished property,” the property that you’re selling.

- “Replacement property,” the property or properties that you’re purchasing through the 1031 exchange.

- “Boot,” the term investors and real estate professionals use to describe any money left over after you perform the 1031 exchange. Think of the Boot as any money that you gain from the sale of your original property that you don’t transfer into a replacement property. Any money left over after an exchange will have a tax liability, so avoid the Boot. If you’re curious to learn more, check out this article on what the boot is and how to avoid it.

- “Qualified Intermediary,” or “QI,” or “Accommodator,” or “Facilitator,” a person that acts as an intermediary qualified to facilitate 1031 tax-deferred exchanges. The main role of the QI is to hold the proceeds from the sale of the relinquished property in an escrow or trust account to ensure you never have actual receipt of the sale proceeds.

- “Exchange Agreement,” a written agreement between the qualified intermediary and the Exchanger (you). This agreement defines the transfer of the relinquished property, the purchase of the replacement property, and the restrictions on the exchange proceeds during the exchange period.

1031 Exchange Rules

The exchange must be between Like-Kind property.

The exchange must be “like-kind,” meaning investment property. This does not include personal residences, property you intend to flip, or securities. This does include property you own as part of a business operation.

Taking control of cash or other proceeds before the exchange is complete may disqualify the entire transaction from like-kind exchange treatment and make all gain immediately taxable.

The IRS draws a hard line here. This rule alone is enough of a reason to hire an experienced real estate attorney and qualified intermediary or exchange facilitator. If you touch any of the cash or proceeds (the “boot”), you’ll be liable for the entire tax bill.

All equity from the relinquished property must be moved into the replacement property.

According to the IRS, the basis (what you paid for the property and all of its improvements) in the replacement property must be the same as the basis of the relinquished property, minus any money received by the taxpayer, plus any gain recognized on the transaction.

For more information on calculating tax basis, check out this article. Please seek qualified advice of a tax attorney when calculating your basis and estimating tax liability.

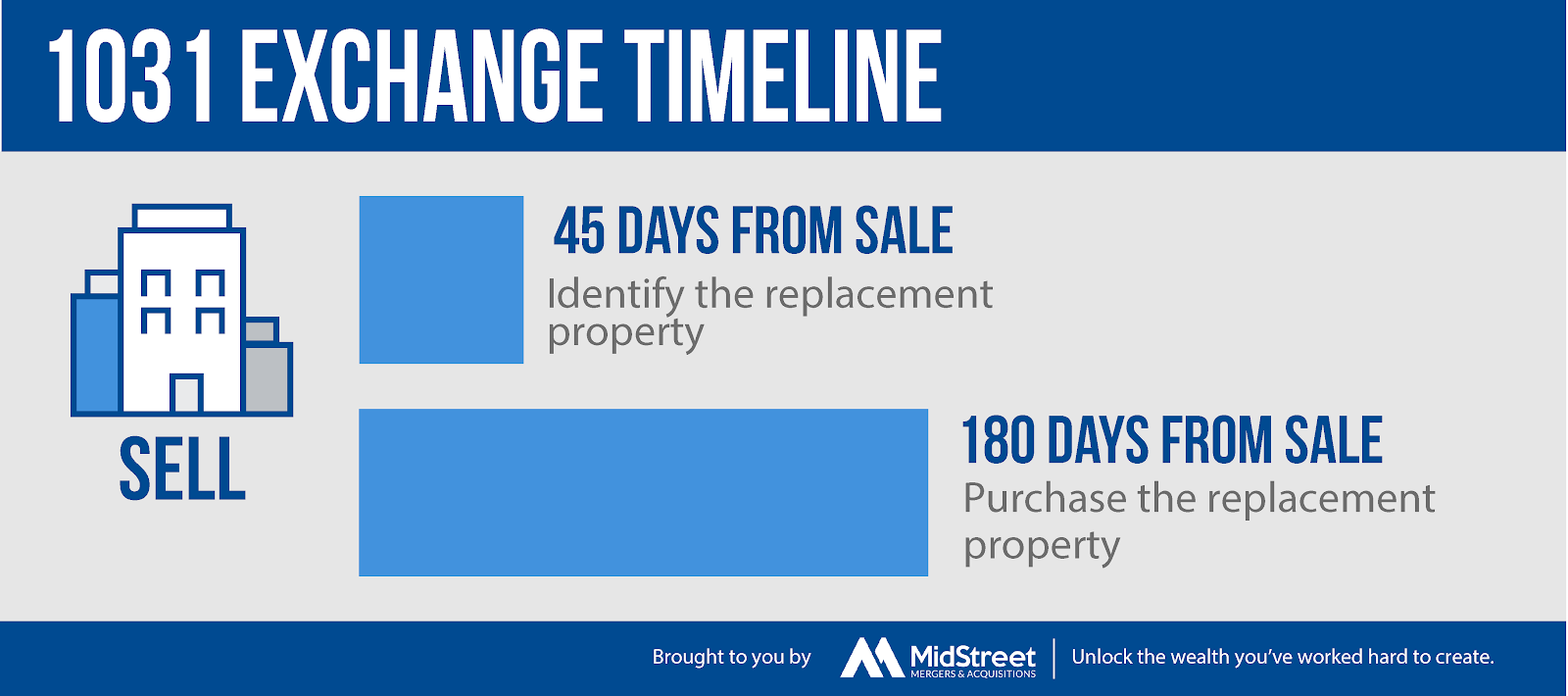

You have 45 days from the date you sell the relinquished property to identify potential replacement property/properties.

According to the IRS fact sheet:

"The identification must be in writing, signed by you and delivered to a person involved in the exchange like the seller of the replacement property or the qualified intermediary. However, notice to your attorney, real estate agent, accountant or similar persons acting as your agent is not sufficient."

You must receive the replacement property and complete the exchange in 180 days OR the date your income tax returns are due.

According to the IRS, to qualify for the exchange, you must receive the replacement property and complete the exchange no later than 180 days after the sale of the exchanged property OR by the date your income tax returns are due for the same tax year your property was sold in. This rule applies to whichever date is earlier.

Three Identification Methods in a 1031 Exchange

There are three identification methods when completing 1031 exchanges and you may choose which one fits your needs the best.

Three Property Method

The three-property identification method allows you to identify up to three replacement properties. You can acquire one, two, or three properties. This rule is most common for business owners and applies to most investors.

200% of Fair Market Value Method

The 200% rule allows you to identify any amount of replacement properties, if their total fair market value isn’t greater than 200% of the fair market value of the relinquished property. Be careful with this rule, as if you break it, the entire exchange could fail.

95% Identification Exception Method

Although it’s an uncommon rule, the 95% rule allows you to identify more than three properties in excess of 200% of the value of the relinquished property. However, you must acquire at least 95% of the value of the properties you identify. This is an unpopular method because it essentially requires you to acquire every property you identify.

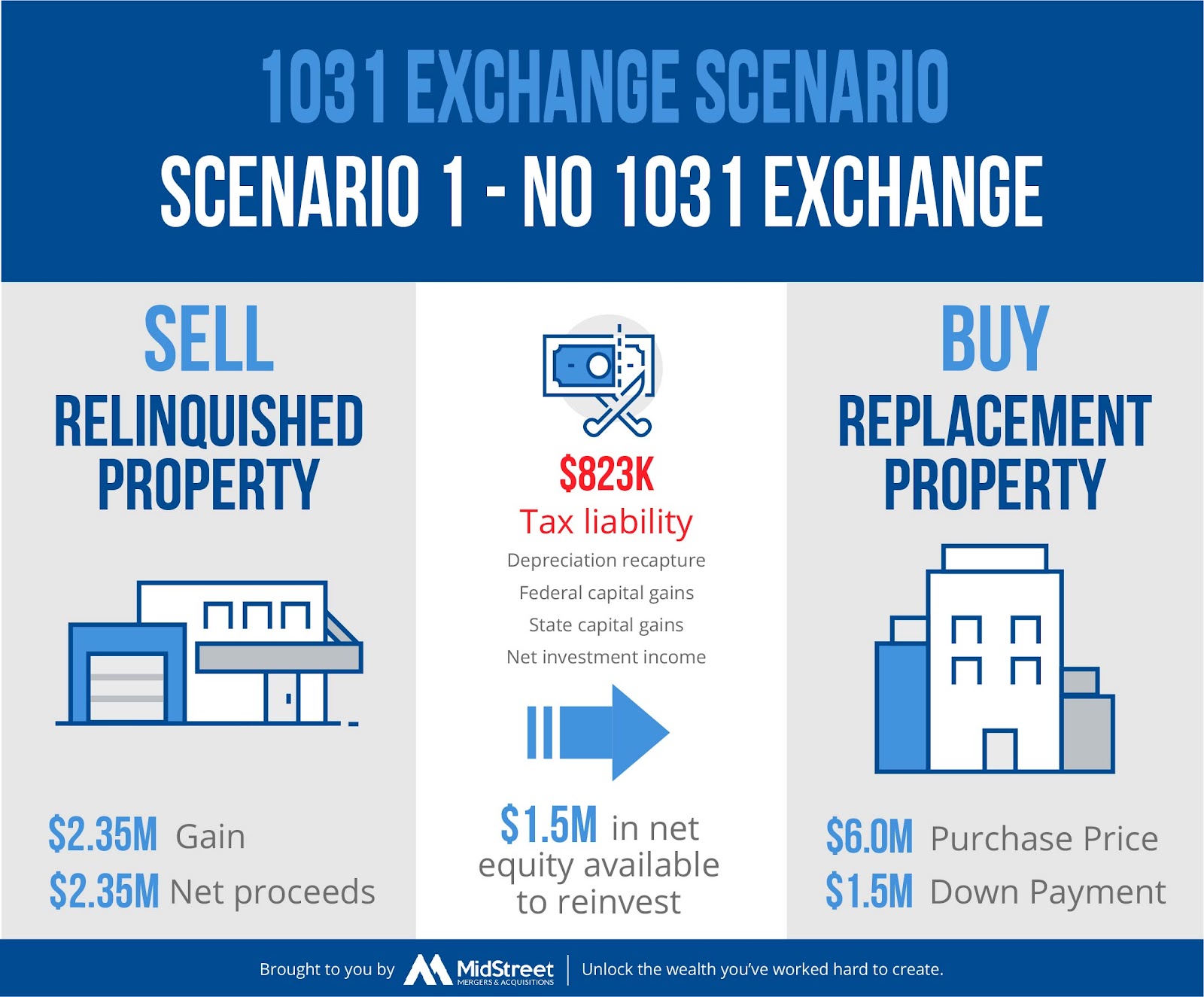

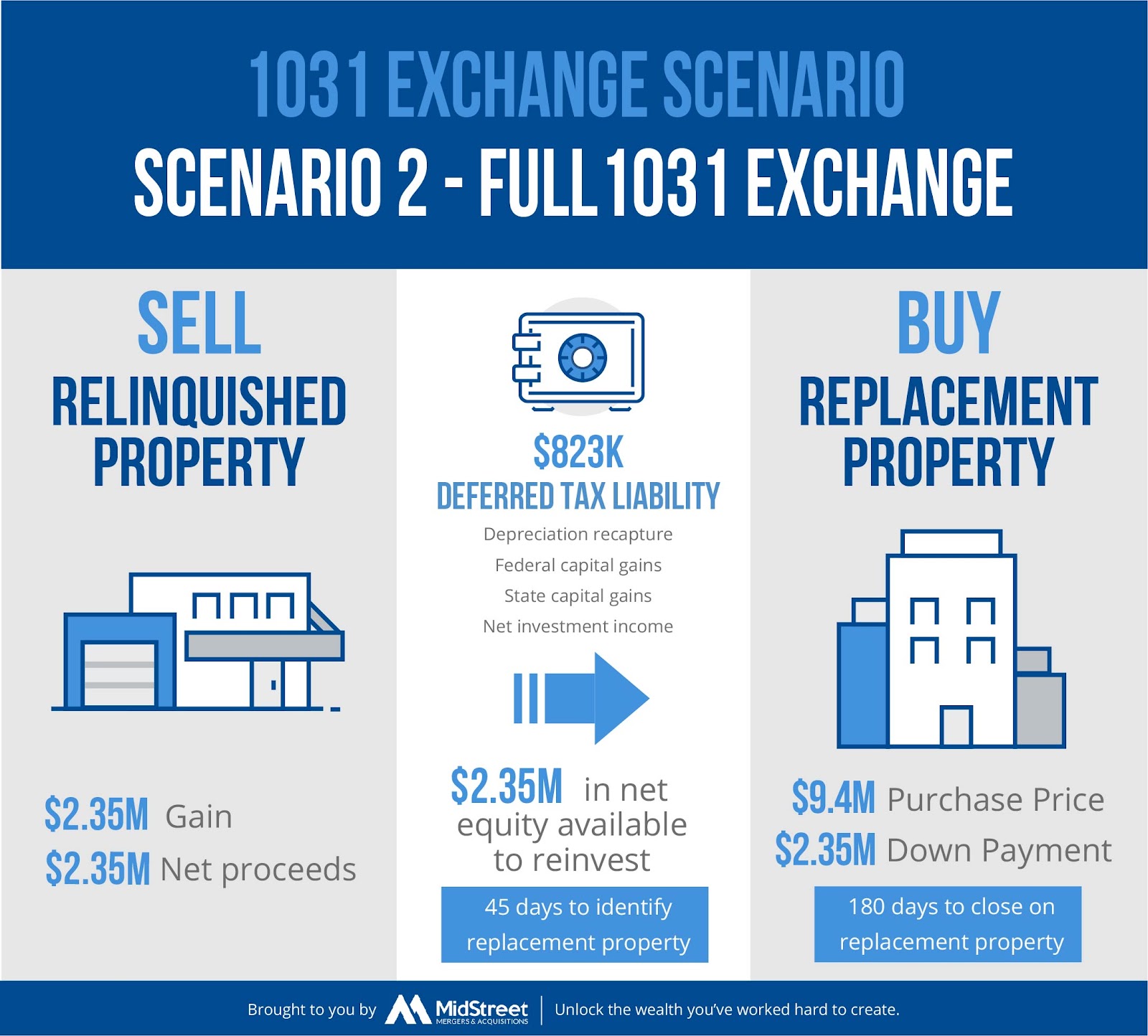

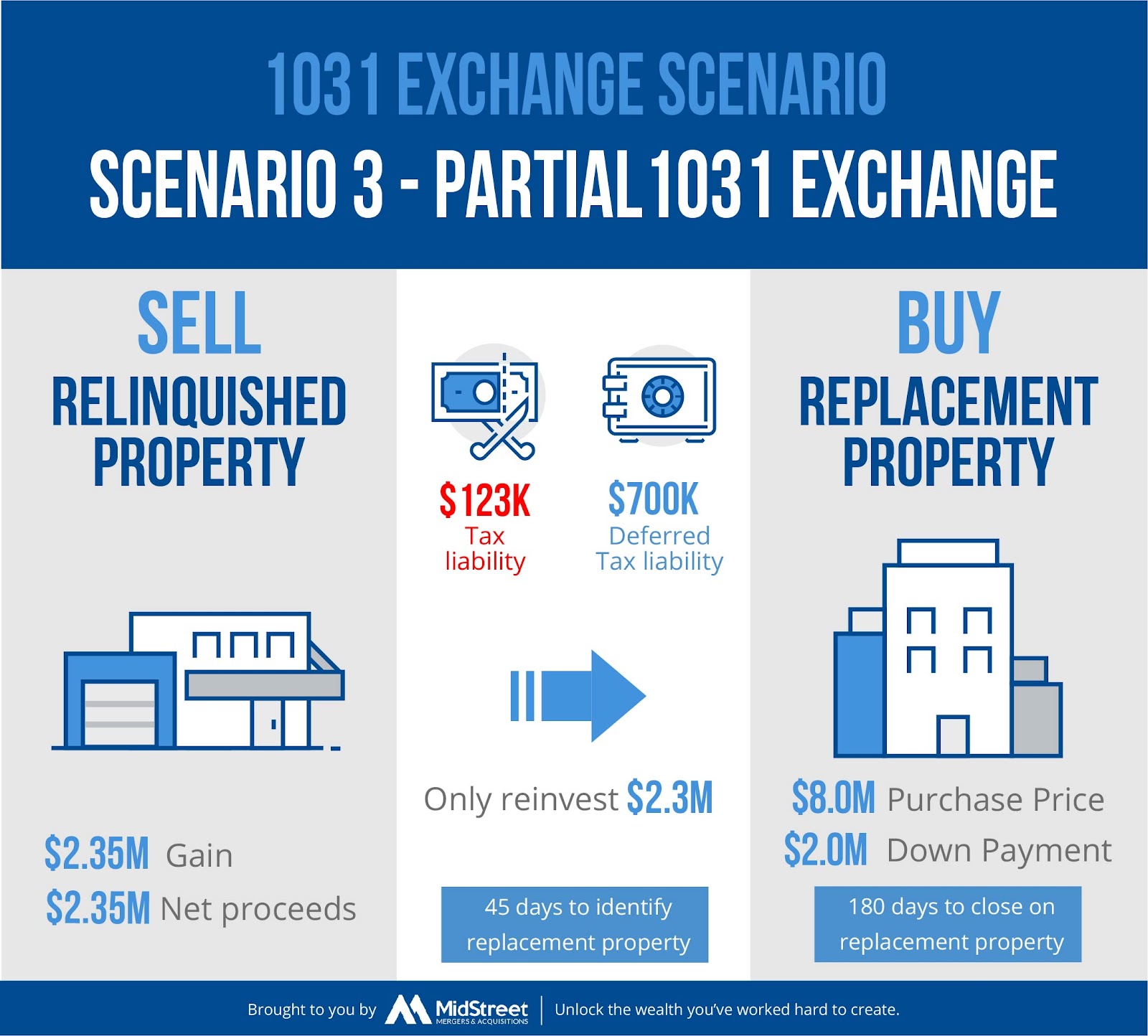

1031 Exchange Example When Selling a Business

The following are simplified examples of 1031 exchanges and illustrate how much benefit deferring your taxes can provide. These diagrams are included for illustrative purposes only – please consult proper legal and tax advice before attempting a 1031 exchange.

How to Make or Break Your 1031 Exchange - Seek Advice from a Qualified Professional

As you’ve likely noticed while reading this article, 1031 tax-deferred exchange – just like selling your business – is complex and structuring one well depends on your unique situation.

Since the rules for the exchange are highly specific and sensitive, having a qualified expert is critical. I recommend hiring an experienced real estate attorney and 1031 exchange intermediary.

45 days to identify a property and 180 days to close may seem like a lot of time. It isn't. It’s critical to plan ahead and assemble a team of professionals to help. Rushing the process creates room for mistakes that could cost you hundreds of thousands of dollars in taxes.

Frequently Asked Questions When Considering a 1031 Like-Kind Exchange

1. What is the definition of Like-kind? Does Like-kind mean I have to reinvest in the same class or type of property?

“Like-kind” property is property of the same nature, character or class. Quality does not matter.

In the eyes of the IRS, the relinquished property and replacement property must meet certain requirements. Both properties must be held for use in a trade, business or for investment.

Most real estate will be like-kind to other real estate, according to the IRS. However, real estate outside the United States is not like-kind to real estate in the United States and visa-versa.

According to the IRS website, certain property types are excluded from section 1031 treatment, including:

- Inventory or stock in trade

- Stocks, bonds, or notes

- Other securities or debt

- Partnership interests

- Certificates of trust

2. How do I compute the basis in the new property?

The IRS recommends that you and your tax representative adjust and track basis properly to comply with Section 1031 regulations. Remember, the taxable gain is deferred, but not forgiven. You need to calculate and keep track of your basis in the new property you acquired in the exchange.

According to the IRS, when the replacement property is sold, if it’s not sold using a 1031 exchange, the "original deferred gain, plus any additional gain realized since the purchase of the replacement property, is subject to tax."

3. Can I purchase more than one replacement property in a 1031 exchange?

You may purchase more than one replacement property, but there are restrictions - refer to the identification methods in the body of this article. If you select the most common option, you can identify up to three properties and purchase one, two, or all three.

4. What is my potential tax liability based on? Taxable gain or equity?

Your tax liability is based on your taxable gain, not your equity.

5. Which type of exchange is right for me: delayed, simultaneous, reverse?

Delayed Exchange

A delayed exchange is when you sell property before acquiring the replacement property.

Most exchanges completed are “delayed.” Delayed exchanges are considerably cheaper than the other types and give you more flexibility in your timeline. I wouldn’t recommend shopping based only on finding the cheapest option – it pays to work with an experienced exchanger.

You must execute a purchase agreement with a buyer for the sale of your property before you can initiate the delayed exchange. Then, your exchange intermediary initiates the sale of the property and holds your proceeds from the sale in a trust/escrow account.

Once the sale is completed, you have 45 days to identify replacement property and 180 days to purchase property you wish to acquire.

Reverse Exchange

A reverse exchange enables you to buy a replacement property first, then sell your relinquished property after the sale is complete.

These exchanges typically cost much more than a delayed exchange and require an exchange accommodation titleholder, which is an LLC created to hold either the relinquished or replacement property. Since you’re creating this LLC, finding a loan could be more difficult since the LLC doesn’t have established credit or history of income.

The time-related rules are slightly different for a reverse exchange. You have 45 days to identify the property you’re going to relinquish, and you have 135 days to complete the sale of that property.

Contact an exchange professional or real estate attorney if you have detailed questions regarding reverse exchanges – their use is beyond the scope of this article.

Simultaneous Exchange

A simultaneous exchange is when you sell the relinquished property and purchase the replacement property on the same day. This exchange is highly sensitive, as any delay in the exchange can result in the exchange failing.

Construction or Improvement Exchange

You might be able to make improvements on the replacement property by using equity from your exchange. Construction/Improvement exchanges can get complicated and are again beyond the scope of this article – seek advice from a qualified professional if you’re curious to learn more.

6. Can I defer part of my taxable gain? What if I can’t find a property with an equal or greater purchase price and equity stake?

You may defer only part of your property’s taxable gain. This is what’s known as a partial 1031 exchange. You might be responsible for:

- The difference in the purchase price of the two properties, if the replacement property is lower in value than the relinquished property. For example, if your original property is valued at $5M, your taxable gain is $1M, and your replacement property’s value is only $4.4M, you will be responsible for paying taxes on $600K.

- Every dollar of equity not transferred to the new property. For example, if you had $1.5M in equity in your relinquished property and only put in $1.2M in equity into the new property, you could be liable for $300K in taxable gain.

7. Do I need an intermediary or an exchange agreement to complete the exchange?

You don’t need an intermediary or exchange agreement to complete a 1031 exchange, but using one is highly recommended. In the Southeast, a typical cost for a delayed exchange is around $1,000. In the long run, the exchanger’s fee could save you hundreds of thousands of dollars in tax liability.

8. How do I report Section 1031 Like-Kind Exchange to the IRS?

I recommend you consult with your tax advisor to ensure you follow the correct procedure. According to the IRS, you must report an exchange via Form 8824, Like-Kind Exchanges, and file it with your tax return for the year in which the exchange occurred.

9. Should I need to use a real estate attorney for a 1031 exchange?

Use of a real estate attorney is not required, but I highly recommend it. Their fee will likely be higher than that of a Qualified Intermediary, but their guidance and advice is well worth their fee.

10. How long do I have to hold the replacement (investment) property? Can I convert the investment property into a personal residence?

The IRS does not define a typical holding period but does emphasize the replacement property must be used for the purpose of investment. Courts have agreed with the IRS by disqualifying exchanges in which the replacement property is sold soon after acquisition (See Black v. C.I.R. 35 T.C. 90 (1960)) and learn more at FirstExchange - Holding Period Requirements In A 1031 Exchange.

11. Can I exchange equity into real property I already own?

Unfortunately, you cannot exchange equity into a property you already own. The rule is for exchanging investment property you own and will sell with new investment property you’ll purchase.

12. Can I purchase a property currently owned by a family member?

You cannot exchange for a replacement property owned by a relative, but you may sell to a relative. The IRS may require both parties to hold their properties for two years after the exchange. Please seek legal and tax counsel if you have questions regarding this issue.

13. I own an investment property with other owners. Can I exchange my partial interest in the property?

You can exchange your partial interest in the property – however, if your interest is not in the property but in a partnership that owns the property, your exchange might not qualify. Remember, partnership interests are excluded from a 1031 exchange.

If everyone wants to sell their property as a partnership, that might qualify as a 1031 exchange. Seek proper legal and tax advice for help on your situation.

14. Can I perform a 1031 exchange on my personal residence also?

Many business owners sell their houses at the same time as selling their businesses. Unfortunately, you cannot perform a 1031 exchange on your personal residence – the IRS is clear that a 1031 exchange is for investment property only.

However, under section 121 of the tax code, if you sell your personal residence and have occupied it for at least two out of the last five years (does not need to be consecutive), up to $250,000 (single) and $500,000 (married) of capital gain is exempt from taxation.

15. Are Qualified Intermediaries (QI) licensed? How do I ensure the money that I use in the exchange is safe and the transaction is handled properly?

There is little regulation governing Qualified Intermediaries. I recommend conducting your own research and due diligence to ensure your exchange funds are held safely protected if the QI cannot provide funds at closing.

A great way to vet these professionals is through word-of-mouth of a professional you trust, such as a skilled CPA or real estate attorney, who will recommend intermediaries they’ve worked with before and trust.

If you don’t have anyone to give a referral, go online, research, and read through their reviews.

16. Can I perform a 1031 exchange with an LLC?

You may perform a 1031 exchange if you own the property through an LLC if you are a Single Member Limited Liability Company (SMLLC), since it’s considered a pass-through to the member (you). Your LLC may sell the original property, and you can purchase the new property in your name. Please consult qualified legal counsel to get advice on your unique situation.

Know Your Company's Worth

Prepare to sell by determining the value of your business.

Subscribe To

THE MIDSTREET BLOG