If you’re thinking about buying a business, you’ve probably started to do some research into the SBA’s 7(a) loan program. You’ve also probably learned that the SBA has some very strict requirements that have to be met before they’ll approve a loan.

One of those requirements has to do with the debt service coverage ratio of the business that you want to purchase. You may be familiar with debt service coverage ratio as it relates to other investments, but for our purposes, we’ll discuss it in the context of a business acquisition.

At MidStreet, we've worked on hundreds of deals involving SBA 7(a) loans so we know what it takes to meet debt service coverage ratio requirements.

In this blog, we’ll teach you everything you need to know about what debt service coverage ratio is, how to calculate it, and why it’s important.

Let’s get to it.

What is Debt Service Coverage Ratio?

In the context of a business acquisition, debt service coverage ratio (DSCR) is a metric used to determine how comfortably a business can make its annual SBA 7(a) loan payment. The higher a business' DSCR, the more money it has left over after making its payments. The money over and above debt service can be used to re-invest into the business and provide for the owners compensation and benefits.

The DSCR is important because it helps lenders understand the level of risk associated with the loan. It should also be considered by a potential business owner as it is an indication of how risky purchasing the may be. If the DSCR is low, it means the business may not be able to cover its loan payments if profits decline, in a recession for instance. This is why the SBA has set a minimum DSCR for all loans.

How to Calculate Debt Service Coverage Ratio

In order to calculate your DSCR, you actually need to calculate some other things first. Your business’s cashflow and its annual loan payments must both be determined before you can start calculating your DSCR.

Let’s take a look at how to calculate each.

How to Calculate Cashflow

To calculate a business’s cashflow, you’ll start with its Seller’s Discretionary Earnings (SDE). SDE is essentially a company’s net income with certain items, like a full-time owner’s salary, added back in order to create a better understanding of the true earnings of the business.

To figure out the business’s cashflow, you will simply remove the amount of an owner’s salary from the seller's discretionary earnings (SDE). Generally, $100k is a reasonable estimation of owner’s salary to deduct. The business’s cashflow is the amount remaining after all expenses (including the owner’s salary) have been deducted from the net income.

Simply put, to calculate a business’s cashflow, you’ll use the formula (SDE – Owner’s Salary ($100k) = Cashflow).

How to Calculate Loan Payments

Once you’ve determined the business’s cashflow, it’s time to calculate an estimate for the loan payments you’ll have to make after closing. This may sound simple at first, but SBA loan payments are a little trickier to estimate than vehicle or home loans. For that reason, we’ve created a downloadable calculator to help you estimate the loan required to purchase the business you’re interested in.

Download our Debt Service Ratio Calculator Below

Putting It All Together

Now that you’ve calculated the business’s cash flow and estimated the loan payments you’ll be making after purchasing it, you can finally arrive at the DSCR.

To calculate the DSCR, you’ll divide the cash flow by the annual SBA 7(a) loan payments. The resulting value represents the business’s DSCR..webp?width=718&name=Cash%20Flow%20(2).webp)

Debt Service Coverage Ratio and the SBA

By this point you may be wondering why so much emphasis is put on determining a business’s DSCR. Sure, it helps represent a business’s financial health, but why is the actual ratio important?

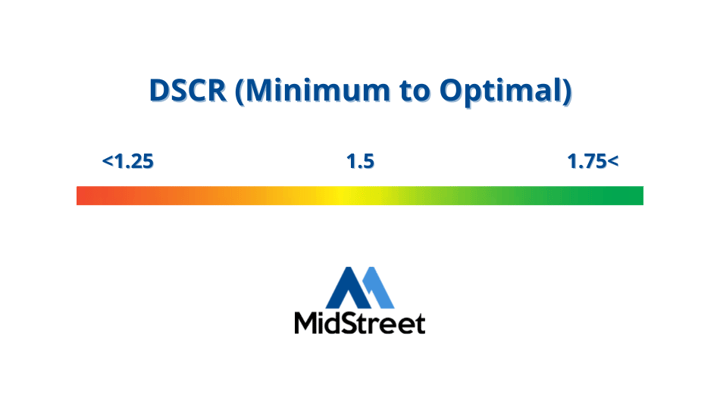

The SBA has a minimum DSCR that a business must have before they’ll approve you for a loan to purchase it. The minimum DSCR requirement to get a loan through the SBA is 1.25, which means that a business’s cashflow must equal 1.25 times its annual loan payment.

Although the SBA only requires a DSCR of 1.25, it’s far more reassuring if that number is 1.5 or greater. The higher the DSCR, the greater security a business has should it incur any major losses, and the more money the owner has to re-invest into the business.

Example Debt Service Coverage Ratio Calculations

To help you better understand how a business’s DSCR is calculated, we’ll take a look at two sample calculations: one that meets the SBA’s minimum, and one that doesn’t.

Example 1:

Let’s say a business’s cashflow is $600k ($700k SDE - $100k owner’s salary). This means that the amount available for loan repayment is $600k.

The annual loan repayment for your business is $400,000.

To get your debt service coverage ratio, you’ll divide the amount available for loan repayment ($600,000 cashflow) by the annual loan payment ($400,000), which gives you a DSCR of 1.5. This meets the requirements set forth by the SBA for borrowers by a margin of .25.

Example 2:

Contrastingly, let’s a business has a cashflow of $320k ($400k SDE - $80k owner’s salary). This means there is $320,000 available for loan repayment. The annual loan repayment is $280,000.

After we do the math ($320,000/$280,000), your DSCR comes out to be 1.14, which doesn’t meet the requirements set forth by the SBA, meaning that the business won’t qualify for an SBA loan at that price.

Think about it. The 1 represents the ability to pay yourself a salary and pay off the SBA loan (a total of $360k). The .14 represents any money left over after loan repayment ($40k).

If the business takes any hits greater than $40k (which isn’t at all uncommon), then there won’t be enough left to pay back your loan, even with a lower owner’s salary.

This is why the SBA implements a minimum DSCR of 1.25: it assures them that you’ll be able to pay them back even if the business goes through a rough year.

Understanding Debt Service Coverage Ratio

To sum it all up, debt service coverage ratio is used to measure a business’s ability to repay its SBA loan after paying an owner’s salary. To calculate DSCR, cashflow should be calculated first.

After calculating the business’s cashflow, you’ll have to calculate its annual loan payment. From there, you’ll divide the cashflow by the loan payment and arrive at the DSCR.

The SBA requires a minimum DSCR of 1.25 which gives them reasonable assurance that the business owner will be able to pay back their annual loan even through declines in profit. A high DSCR means that a business has greater security should it go through a decline in profits and offers the opportunity to re-invest more money into the business.

If you’re looking to acquire a business, but aren’t sure how to best estimate its DSCR, feel free to contact us today. We’d love to speak with you about your interest in one of our listed businesses or further explain how to calculate debt service coverage ratio.

Know Your Company's Worth

Prepare to sell by determining the value of your business.

Subscribe To

THE MIDSTREET BLOG