Imagine you’re talking to your financial advisor and they say “I think this is a great investment! You can buy this business for $1,000,000 and you’ll make $40,000 a year operating it.”

You would probably question your choice in financial advisor at that point. But, this is a real consideration when you’re looking to acquire or sell a business: how much and what type of cash flow does your business generate?

You might have heard that cash flow is the primary determinant of business value. This is true, but the metric you use to measure cash flow is important to the value as well.

At MidStreet, we help business owners understand cash flow to value their company and help buyers understand how cash flow affects what they will put in their pocket after all is said and done.

In this article, we’re going to compare cash flow to seller’s discretionary earnings (SDE) and discuss how it impacts both buyers and sellers.

Let’s hop in.

What is Cash Flow?

Cash flow is the net amount a business owner puts into their pocket at the end of the year. This is the money that is left over after they have paid off loans, capital expenditures, and other expenses. It is the amount they will take as a distribution from their LLC or corporation plus any wages they received during the year.

An important thing to understand about cash flow is it differs from net income on your balance sheet because net income includes non-cash expenses like depreciation and amortization. Cash flow includes the actual cost of capital expenditures rather than depreciation, because depreciation might not accurately represent your actual spending on new assets.

An easy way to calculate cash flow is to take your SDE and subtract capital expenditure and any loan payments. This gives you an idea of what profit your business produces after all expenses are paid.

What is SDE?

Seller’s Discretionary Earnings is the amount one owner-operator earns from running a business. The SDE of a business represents the “recasted” or “normalized” financials to show investors and potential buyers how much they could earn from the company.

Calculating your business’s SDE can be more complicated than other metrics - so we put together a guide on SDE here.

The best way to calculate your business’s SDE is to take your net income off of your most recent tax return preferably, and add back certain expenses. There are two types of add-backs: standard and situational. Use our guide to determine what your add-backs will be, there are a lot of factors to consider.

How do Cash Flow and SDE Differ?

The simplest way to think about cash flow is starting with SDE and adding in a couple of balance sheet items to better understand how cash is moving in your business.

A couple of key differences between SDE and cash flow:

Capital expenditures - To accurately assess the cash flow of the business, you will need to remove all capital expenditures. These include purchases of things like machines, equipment, and vehicles.

Loan payments - If your business has loan payments they would be subtracted from the SDE to find cash flow. This is because SDE is before financing and cash flow is after.

You can use the SDE as a base for finding the true cash flow of the business. The theory is that you will remove these items to show the cash flowing in and out of the business, not just the financial benefit to one owner-operator (like SDE shows).

How Cash Flow Impacts Financing and DSCR

If you’re buying a business with an SBA 7(a) loan, the lender will calculate the debt service coverage ratio when underwriting your deal. The debt service coverage ratio (DSCR) shows the profit of the business in relation to the cost of the loan.

Lenders are looking for a DSCR of at least 1.25x. If the DSCR is close to 1.0x, that means the business will produce just enough profit to break even when paying the loan back each year. DSCR’s that are closer to 2.0x indicates that the business has flexibility to handle their loan payments.

Some lenders will use cash flow to determine your DSCR and others will use SDE. They will choose to use SDE or cash flow based on the industry your business is in. If it is a capital-intensive industry, such as trucking, they are more likely to choose cash flow.

They would remove capital expenditures and the increase in working capital to understand how your business needs to use cash to operate. In all cases, SBA lenders remove the buyer's salary from the SDE/cash flow before calculating the debt service coverage ratio to ensure his or her bills are paid first.

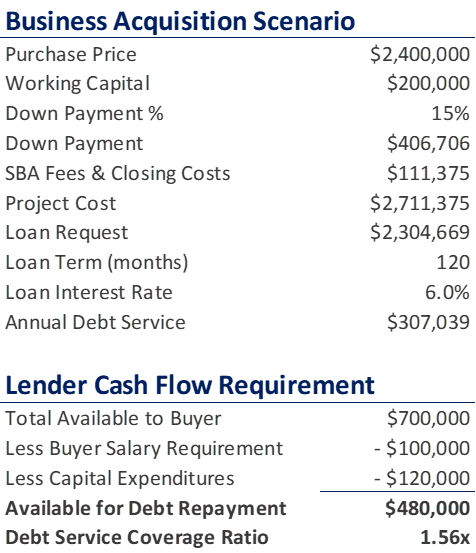

Example of Calculating Cash Flow of a Distribution Company

Say you own a distribution company that does $7 million in revenue and earns $700,000 in SDE. The buyer that wants to purchase the business has bills (mortgage, car payment, etc) of $100,000 per year.

The first thing the bank is going to do when calculating the debt service coverage ratio is to subtract the buyer’s estimated bills ($100,000) from the SDE ($700,000). Now, assume your business has to spend $120,000 per year on capital expenditures like new vehicles and equipment.

The bank will subtract the capital expenditures from the SDE because the buyer will have to pay these expenses before paying the loan. Then, the bank will take this new figure ($480,000) and divide it by the annual loan payments of $307,039 to find the debt service coverage ratio.

$480,000 / $307,039 = 1.56 (DSCR)

How Can You Increase Your Cash Flow?

Consistent, positive cash flow increases the chance of an owner being able to successfully sell their business. It also increases the chance of the buyer being able to receive financing to pay for the business.

So how can you increase cash flow in a business as an owner?

To increase cash flow, you can:

- Shorten your payment terms with customers and incentivize them to pay earlier (reduce your accounts receivable).

- Extend payment terms with suppliers - prove you’re credible and will pay them to get better terms. Avoid cash-on-delivery suppliers.

- Reduce CAPEX (capital expenditure) by maintaining equipment and buying the most cost-effective pieces of equipment.

- Finding which jobs and products produce the highest margin and choose to focus on those jobs. Revenue is great but cash flow is king when it comes to business sales.

By increasing the cash flow of a business, an owner not only makes it more attractive to buyers, they also improve their internal operations.

Understand Why Cash Flow is Important in The Sale of a Business

Cash flow in a business impacts both the buyer and seller, which is why knowing how it is calculated and how it affects you can benefit you in a business sale.

If you are a buyer that wants to learn more about purchasing a business, read “How to Buy a Business Using the SBA 7(a) Loan Program (With Example).”

If you are a seller that wants to know more about valuing your business, read “SDE vs EBITDA: What's the Difference?”

Understanding the financial components of buying and selling a business can be difficult, especially if this is your first time. To get help understanding how cash flow impacts a sale, contact us today.

Know Your Company's Worth

Prepare to sell by determining the value of your business.

Subscribe To

THE MIDSTREET BLOG